It’s time: you need to tune your scanner for information coming out of Mexico. What has always smoldered has started to flame. Those flames could be a five-alarm fire in 2018. Hyperbole? Maybe, but in the course of over fifty visits to Mexico this year alone and 33 years in the country focused on the economic and financial environment in the country, it is clear to our firm that the country is at a critical juncture, and the presidential elections next year will be the determining factor of which way Mexico turns.

Candidates

Unfortunately, rhetoric coming from President Trump has weighed greatly on the populace, going a long ways to aid the populist candidate. If the elections were held today, there is little doubt that the radical populist Andrés Manuel Lopez Obrador (“AMLO”) would be elected and the result could be quite negative.

In our most recent trip, we spent time with a couple of candidates and were on hand for the announcement of the PRI party’s official candidate – Jose Antonio Meade. In a normal cycle, these individuals would be viewed as relatively strong candidates and possible leaders. In the current environment, however, the country is fixated on the negativity coming from Washington related to trade generally and NAFTA specifically.

Investment in the country has slowed and risks are rising. Foreign Direct Investment has dropped from $3.9 billion USD for the 12 months ending December 31, 2012 to $491 million USD for the 12 months ending September 30, 2017. Add to that hostility regarding border and immigration issues and the momentum seems unstoppable for AMLO. While AMLO has been compared to Hugo Chavez, it is not necessary for him to be entirely alike in order to set the country back. Coalitions are building and there may be a way to stem the tide, but that is unlikely as long as so much Mexican-focused negativity emanates from Washington.

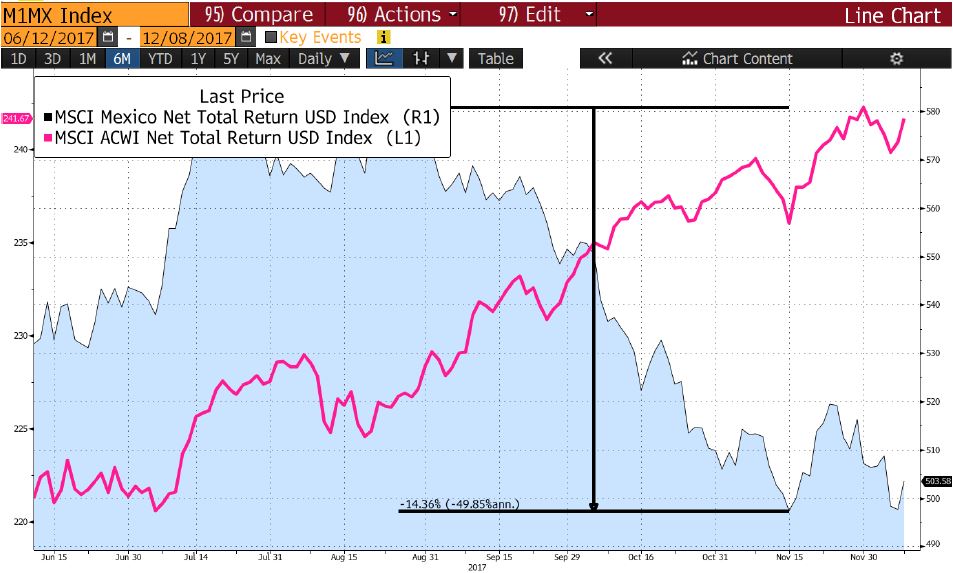

Fortunes have been won and lost in the extreme environments seen in Mexico over time. Crises have wiped out wealth for many while others have built empires. Now is the time to tune in your scanner; attentiveness to the issues at hand is imperative. Our view currently is to be naked any exposure to Mexican assets. This has been beneficial as the momentum of the MSCI Mexico Index has significantly underperformed other markets in the ACWI (2nd worst USD price return over the last 3 months, down 11.4%).

Over the course of the next twelve months, however, there may be a chance to take positions that could reward long-term portfolios.

We are trying to thread a tight needle with our outlook, but the view driving our strategy contemplates AMLO winning the election on July 1. Given the stakes and potential loss of power of the ruling party, there could be considerable upheaval and asset price discounts as the election is contested and results not final for a period of time. The markets will have awoken to this possibility leading into the election and will begin talking about the outcome being a Chavez-lite result. Already cheap markets would look even cheaper in this scenario. The current Price to Earnings ratio (P/E) for Mexico is 16.8x. This P/E ratio is 6.4x less than Mexico’s 5 year average P/E ratio of 23.2x, and represents the largest “discount” of all the countries we follow in the ACWI. The Bolsa will decline further and MXN will weaken if indeed AMLO is declared the winner, but Mexico’s current valuations (versus its own history) suggests that a good portion of political risk has already been priced in.

Without trying to pick the bottom, we will build meaningful positions at these lower levels given a fairly broad and time-insensitive view. While conditions are different than Brazil in 2002, the general panorama in Mexico could be similar to the Lula election with Brazilian stocks down nearly 80% in USD terms going into the election, but sprinting over 1900% in USD terms to the upside over the course of several years.

We believe that AMLO will be prudent, at least relative to expectations – more Lula than Chavez. As Mayor of Mexico City was generally considered to be pragmatic and flexible when working with business. While Mayor, he built freeways and worked with business leaders to restore the city’s historic center.

He is likely to roll-back energy reform, push hard against the U.S. while looking for new partnerships, including exiting NAFTA which would place Mexico under WTO rules which would be more favorable for Mexico, and raise taxes significantly on the rich. But he will be attentive to the economy broadly. The country has always benefited from a weak currency and its proximity to the U.S. which will perhaps payoff nicely under WTO rules. Companies will have the ability to grow earnings. Currently, due to the uncertainty, the market is over-looking very strong expected earnings growth. Consensus forecasts suggest EPS growth of 23.8% annually over the next 3 to 5 years, outpacing the expected earnings growth of 13.1% for the average country. If AMLO takes power smoothly and uncertainly declines, Mexico’s high growth potential and attractive valuation will attract global investors and support asset prices.

Mexico is 0.4% of the ACWI. This is not a market that will make or break your year if you have a global mandate. The moves could be big enough, however, that keeping close eye on the political scene in 2018 could add improve your ability to outperform next year. Mexico is a mature country with great people, culture, history (and of course food) and it will bounce back strongly as it always has after crises. Our bet is that there will be a repeat of this kind of scenario; so tune in and stay tuned!