5/12/18: Bulls back in control?

2018 is nothing like 2017. I’m older, in worse shape, and equity returns are much harder to come by. If you’re an equity manager forced to invest in anything other than growth stocks, you’re really not having a fun year thus far. Thankfully, I’m part of a team of investors who understand being “style-stubborn” simply offers you less options to beat the market. Beating the market is still a “thing” right? I’ve written a few times that my base case for the economy and the economic data that tracks it will mostly be LESS GOOD from here. That doesn’t mean the data will be bad or a recession is near. Our research simply indicates that virtually all of the important economic data is currently at levels that indicate “the best of times” and historically the forward returns are less robust. The data is the data. A week ago, every investor, trader, and strategist was talking about the current pattern of the S&P 500. A wedge had formed and as prices bounced around inside the narrowing channel, the pressure was building for a bigger move. As I write this commentary, the move appears to be UP. My biggest concern wasn’t the markets technical pattern, it was and continues to be the possibility of peak growth colliding with the rising costs of virtually everything we want and need as consumers. Another significant worry: forward expectations appear quite lofty. Analysts are often too bullish at tops and too bearish at bottoms. Via Factset, here’s the current set-up headed into Q2 earnings that begin in early July. My history lessons show that we saw this kind of sustained earnings & revenue growth only one other time in the last 30 years, the late 1990’s. We averaged 4%+ GDP during that period and we currently don’t seem to be able to get a full year over 3%. Maybe it’s different this time.

For Q1 2018, companies are reporting earnings growth of 24.9% and revenue growth of 8.2%. Analysts currently expect earnings to grow at double-digit levels for the remainder 2018.

For Q2 2018, analysts are projecting earnings growth of 18.8% and revenue growth of 8.3%. For Q3 2018, analysts are projecting earnings growth of 20.9% and revenue growth of 7.1%. For Q4 2018, analysts are projecting earnings growth of 16.5% and revenue growth of 5.7%. For all of 2018, analysts are projecting earnings growth of 19.2% and revenue growth of 7.2%.

WHY AREN’T PEOPLE TALKING ABOUT THE REVENUE GROWTH PEAK THAT APPEARS ABOVE? MARKETS TEND TO BE FORWARD-LOOKING, WHEN WILL IT MATTER?

Fortunately, we have plenty of tools at our disposal to adapt to changing market & economic conditions.

For now, bulls appear to be back in control

Now is a good time to remember why we invest our capital. For most of us, we take risk in the hopes of receiving a decent return and we prefer to have a ride that’s not too volatile. Every asset manager has its own strategy to accomplish this and we are no different. We prefer to focus on an enormous and predictable theme, consumer spending. In the U.S., consumer spending is a $12 trillion per year phenomenon and globally it’s 60% of GDP or roughly $40 trillion per year. We invest in the theme via the most relevant and leading Brands that appear to be best positioned. We also spend an enormous amount of time analyzing what’s driving S&P 500 returns so we can make sure we own sufficient exposure to the brands and style factors that are being rewarded most. This research offers us a significant portfolio edge. We also give ourselves significant flexibility to adapt to whatever the market throws at us. I cannot say that about most equity mutual funds and virtually all ETF’s.

The vast majority of these are forced to be fully invested through good times and bad and are focused on managing in one “style” (value, growth, dividends, large cap, etc). In our opinion, that limits a funds ability to outperform on a more consistent basis. We chose to adopt a “more ways to win” investment approach.

Our job as allocators is quite simple, the execution of those goals, often complex:

1.) Beat the market. Not over a full market cycle but every year. Goals are just that, goals.

2.) Protect capital while offering a much smoother ride during economic slowdowns.

I feel confident volatility will be with us for the rest of 2018 but it will likely come in spasms. There’s clearly a lot to be thankful for as well as be fearful of. We are always one China tariff related, Trump-tweet away from the market giving up the bulk of its recent gains. If the Fed decides to ramp up its interest rate hikes into a potential earnings peak, markets will not fare very well. Please call me when there’s nothing to worry about, then I’ll be really worried. Until then, its business as usual and we will continue to allocate to the best 25-50 brands from within our Brands Index that give us the best chance at beating the market.

2017 & 2018 YTD have been simple: overweight growth stocks or lag badly. We think the narrative will change as we move through the year. The Dynamic Brands strategy is significantly overweight the leading growth brands but the portfolio is also balanced by its increasing allocation to the stable, predictable brands from Consumer Staples and Specialty REITS. Our team at Accuvest feels quite good about this current portfolio barbell. Consumer Staples are not all the same. We are focused on the brands we believe have low expectations, high and sustainable dividends and accelerating cash flow and sales. We also are not believers that interest rates will rocket higher from here. If growth is about as good as it gets, rates are likely closer to the top end of the range for now. That’s what makes us comfortable with owning “bond proxies” at this part of the cycle. If growth does indeed slow from here, the defensive brands should act as a portfolio stabilizer later this year. In the meantime, we collect attractive dividends from a group of companies loathed by investors. We like that set-up a lot.

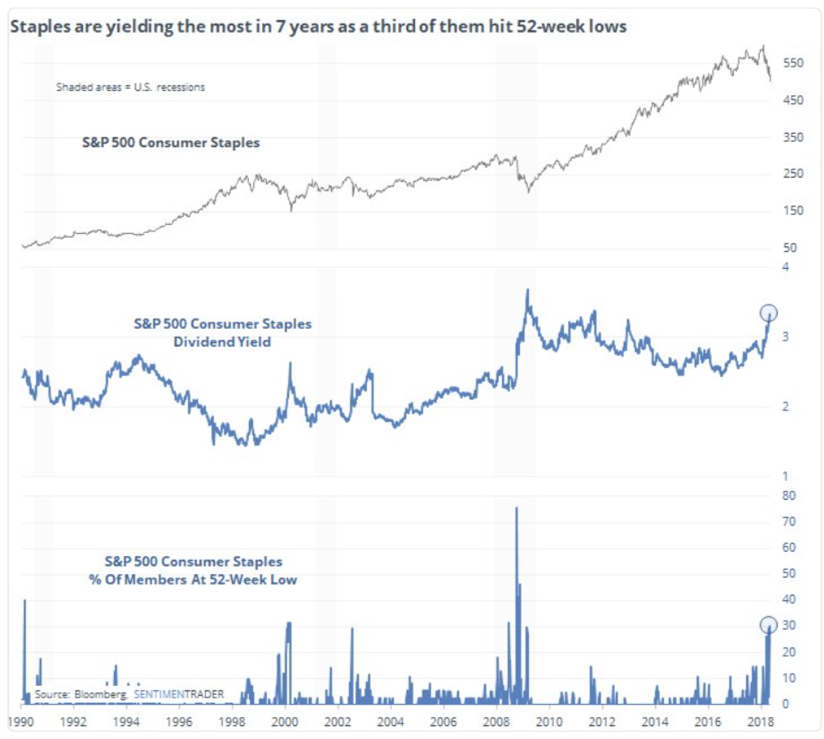

Below is a chart from sentimentrader.com highlighting the current set-up for Consumer Staples in aggregate. They are now yielding more than they have in 7 years as a third of the sector hits 52-week lows. There’s always some opportunity on the 52-week low list. Particularly when combined with many of the greatest brands at or near the 52-week high list.

Imagine a world where every manager had full flexibility to invest in leading companies, serving a large and important theme, had the ability to dial-up or down risk taking and was agnostic to value or growth, domestic or international, mid or large, and could hold copious amounts of cash if the environment warranted it. I’ll stick my neck out and say that would be a world where the average active equity manager would beat his benchmark at a much more impressive rate than the current industry data indicates.

Portfolio edge #1: Top brands have historically been superior performers.

I could show an illustration of our Index (Alpha Brands Consumer Spending Index) looking backward but some would view that as self-serving so I’ll offer some 3rd party validation of a “brands-focused” investment universe. The largest ad agencies and PR firms have been highlighting the power of top brands for decades. Their track record of success being superior companies and stocks is not disputable.

Below is information from BrandZ, a subsidiary of global ad agency, WPP. Their Top 100 Global Brands list has a stellar track record of outperforming the MSCI World Indices. Again, this is for illustrative purposes only and you cannot invest directly in an Index, nor can you invest directly in the BrandZ portfolio. Here’s the full report link, it’s a terrific read. BRANDZ: MOST VALUABLE GLOBAL BRANDS 2017

Additional evidence of Brands being superior performers comes from the Interbrands, Global Top 100 Brands list. Interbrands is a subsidiary of Omnicom, one of the largest ad agencies in the U.S. Brands Matter. Link & source here: INTERBRANDS: BEST GLOBAL BRANDS 2017

Portfolio edge #2: Significant portfolio flexibility

If you’re goal is to beat a benchmark, does it make sense to analyze the strengths and weaknesses and build a strategy that exploits those weaknesses? We think so. One way we accomplish this is by studying what’s driving the returns within markets via tracking “style factors”. Are the returns coming from a small group of companies currently? YES: Growth stocks are significantly outperforming value stocks. When growth is scarce, investors are willing to pay more for an asset that is scarce. By the way, the current growth-over-value cycle is VERY long-in-the-tooth, which offers absolutely nothing in the way of timing the mean reversion.

One day, value will start outperforming, the downtrend will break and value will outperform for many years. If you don’t track that factor, how will you know when it happens? If you’re stuck investing in growth when the cycle turns, how will you add value?

Exhibit A: What types of companies are performing well now?

The screenshot below highlights the performance of the highest ranked 25% vs lowest ranked 25% from within our Brands 200 Index. The story has remained consistent for now: Returns are coming from: Superior operators (operating kings), low debt brands, higher beta brands, high sales growers with lower margins (room for margin expansion), Low sales (room for expansion) and those that are investing aggressively for the future via high R&D expenses. When you’re willing to do the work, you can always find an edge.

Exhibit 2: Top 50 ranked Brands using each style factor, rebalanced quarterly using our Brands 200.

SOURCE: ACCUVEST RESEACH

Bottom Line:

The equity markets are a wonderful place to invest for long-term gains. To get those gains, however, one must accept a certain amount of risk along the way. The business cycle always matters and the data is flashing a “as good as it gets” sign. It will matter when it matters. We believe the emergence of volatility is a preview of what may lie ahead as the cycle gets older and older. We currently do not see the signs of an imminent recession however.

The data is very clear with regard to investments. Most active, equity funds & ETF’s are terrific for bull markets because they must be mostly fully invested at all times, by prospectus or ETF rules. Generally, they tend to struggle in sideways markets and perform dreadfully in economic slowdowns. Why? A key reason is most equity managers are “style stubborn”. They manage assets by owning a narrow group of companies: large-cap, mid-cap, small-cap. Deep value, relative value, GARP (growth at a reasonable price), high growth. High dividend, dividend growth, low volatility, etc. The market rotates over time and styles go in and out of favor. If you are forced to wait your turn for your style to go “in favor”, you are by definition forced to go through periods of time when your style is out-of-favor and underperformance is the outcome. We think there’s a better approach.

One day our growth-tilted Dynamic Brands portfolio will pivot from a growth-tilt to a value & dividend tilt. The portfolio will normally vacillate between fully invested, holding excess cash, to shifting to fully balanced and highly defensive. The business cycle warrants it, common sense demands it.

Consumer spending will always be the primary driver of our economy but different brands will be best positioned according to where we are in the business cycle. Our style-factor work helps us determine which part of the lake to fish in and our macro work helps us determine how much exposure to risk is prudent at any given time. We firmly believe, in aggregate, this is a much better framework than most other firms allow themselves to utilize.

From all of us at Accuvest Global Advisors, we thank you for your trust & support in us and we look forward to managing your assets through good times and bad by adapting to markets via the most powerful brands.

DISCLOSURE:

This information was produced by and the opinions expressed are those of Accuvest as of the date of writing and are subject to change. Any research is based on Accuvest proprietary research and analysis of global markets and investing. The information and/or analysis presented have been compiled or arrived at from sources believed to be reliable, however Accuvest does not make any representation as their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated therein. There are no material changes to the conditions, objectives or investment strategies of the model portfolios for the period portrayed. Any sectors or allocations referenced may or may not be represented in portfolios of clients of Accuvest, and do not represent all of the securities purchased, sold or recommended for client accounts.